How to Achieve Financial Freedom in 2026: Your 6-Step Roadmap

To achieve financial freedom 2026, you need to understand that financial freedom means different things to different people.

For some, it’s the ability to retire early. For others, it’s simply having enough saved to handle life’s uncertainties without panic.

But regardless of how you define it, one truth remains: financial freedom doesn’t happen by accident. It happens when you take deliberate, consistent steps toward building the kind of financial security that lets you make choices based on what you want—not what you can afford.

The path to achieve financial freedom in 2026 starts with understanding that this isn’t a quick transformation. It’s a systematic process built on solid money habits, realistic expectations, and a clear understanding of how saving, investing, and tax efficiency actually work together.

This guide walks through six high-impact actions you can take this year to build real financial stability.

Each step includes practical frameworks you can use immediately, realistic timeframes for results, and honest assessments of what works—and what doesn’t.

Important disclaimer: This content is educational only and does not constitute financial advice. Individual circumstances vary significantly, and decisions involving investments, taxes, retirement accounts, or debt management should be made in consultation with qualified financial professionals. Past performance does not guarantee future results, and all investments carry risk of loss.

Step 1: Build Your Emergency Fund to the Right Size

An emergency fund is the foundation of financial stability.

It’s the buffer that prevents a car repair, medical bill, or unexpected job loss from derailing your entire financial plan.

Most financial advisors recommend keeping 3-6 months of essential expenses in an immediately accessible account. That’s rent or mortgage, utilities, groceries, insurance, minimum debt payments—not your full lifestyle spending.

Why This Matters More Than You Think

Without an emergency fund, unexpected expenses force you into high-interest debt.

Credit card interest rates currently average 20-24% APR. Personal loans range from 10-36% depending on credit scores.

When you have to borrow for emergencies, you’re not just paying the original expense—you’re paying that expense plus interest, which compounds your financial stress and delays your progress toward actual wealth building.

The Math Behind 3-6 Months

Start by calculating your true essential monthly expenses.

If your essentials total $3,000 per month, you need $9,000-$18,000 in your emergency fund. That sounds like a lot, but it’s built gradually.

Most people take 12-24 months to fully fund their emergency reserve, adding $200-$500 per month until they hit their target.

Where to Keep Emergency Money

Your emergency fund should be in a high-yield savings account or money market account.

As of early 2025, competitive rates range from 4.0-5.0% APY at online banks. This doesn’t beat inflation, but it keeps your money liquid and immediately accessible.

Traditional brick-and-mortar banks often pay 0.01-0.50% on savings, which is why online banks make more sense for this purpose.

Critical limitation: Even at 5% APY, your emergency fund loses purchasing power over time if inflation runs higher. This is why you only keep true emergency reserves in cash—everything else should eventually be invested for growth.

Common Mistakes to Avoid

Don’t keep your emergency fund in checking accounts that pay zero interest.

Don’t invest emergency money in stocks or bonds—you might need to access it exactly when markets are down.

Don’t count credit cards as your emergency fund. Access to credit is not the same as having cash reserves, especially if your income drops and you can’t make payments.

Quick Summary

- 3-6 months of essential expenses is the target

- High-yield savings accounts (4-5% APY) are the right vehicle

- Most people take 12-24 months to fully fund this

- Cash loses to inflation, so only emergency money stays here

- Credit access is not a substitute for actual savings

Step 2: Build Monthly Investing Habits to Achieve Financial Freedom 2026

Once your emergency fund is established, the next step toward financial freedom is consistent investing.

This is where you actually build wealth over time—not through savings accounts, but through market-based growth.

Why Monthly Investing Works Better Than Timing

The biggest mistake people make with investing is waiting for the “right time” to start.

They watch the news, worry about market highs, fear corrections, and ultimately do nothing while years pass.

Dollar-cost averaging—investing the same amount every month regardless of market conditions—removes the guessing game. You buy more shares when prices are low, fewer when prices are high, and over time, this averages out to solid long-term returns.

The Real Timeline for Investment Growth

Here’s what most people don’t tell you: investing takes time to work.

In the first 1-2 years, you’re mostly just seeing your own contributions accumulate. The compounding hasn’t kicked in yet.

By years 3-5, you start seeing meaningful growth from returns on your earlier investments.

By years 10-15, the compounding effect becomes dramatic—your money starts making more money than you’re contributing.

To achieve financial freedom in 2026, you need to accept that this year is about building the foundation, not reaching the finish line.

What to Invest In: The Basics

For most people, low-cost index funds are the most effective long-term investment vehicle.

These funds track broad market indexes (like the S&P 500) and provide instant diversification across hundreds of companies.

Total stock market index funds typically charge 0.03-0.10% in annual fees, compared to 0.50-1.50% for actively managed funds. Over 30 years, that fee difference costs you tens of thousands in lost returns.

Risk reality: Stocks can lose 20-40% of their value in a single year during recessions or market corrections. This is normal and expected. If you can’t handle seeing your account balance drop temporarily, you need a different investment mix—possibly including bonds, which are less volatile but also provide lower long-term returns.

Tax-Advantaged vs. Taxable Accounts

Most investment growth happens inside retirement accounts: 401(k)s, IRAs, Roth IRAs.

These accounts offer either tax-deferred growth (traditional accounts) or tax-free growth (Roth accounts), which dramatically increases your long-term wealth compared to taxable brokerage accounts.

2026 contribution limits:

- 401(k): $23,000 ($30,500 if age 50+)

- IRA/Roth IRA: $7,000 ($8,000 if age 50+)

If you’re not maxing these out, that’s your first priority before investing in taxable accounts.

Practical Tool: Monthly Investment Allocation Framework

Copy this framework and adjust to your situation:

If household income is under $75,000:

- Emergency fund until 3 months saved: 100% of investing budget

- After emergency fund: 401(k) to employer match → Roth IRA → Additional 401(k)

If household income is $75,000-$150,000:

- Emergency fund until 6 months saved: 70% of investing budget

- Simultaneous Roth IRA contributions: 30%

- After emergency fund: Max Roth IRA → Max 401(k) → Taxable brokerage

If household income is over $150,000:

- Emergency fund: 3 months minimum (higher income = faster replacement if needed)

- Max 401(k) and backdoor Roth IRA simultaneously

- Taxable brokerage for amounts beyond retirement limits

This is a starting framework only. Individual circumstances—debt levels, age, risk tolerance, specific goals—require personalized adjustment.

Quick Summary

- Monthly investing beats trying to time the market

- Meaningful compounding takes 3-5 years to become visible

- Low-cost index funds are the foundation for most people

- Tax-advantaged retirement accounts should be maxed first

- Stocks can drop 20-40% in bad years—this is expected, not a failure

Step 3: Make Your Retirement Accounts Work Harder

Retirement accounts are the most powerful wealth-building tool available to most Americans.

The tax advantages are significant, but most people leave money on the table by not using these accounts effectively.

Understanding the Tax Advantage

Traditional 401(k)s and IRAs give you an immediate tax deduction.

If you’re in the 24% tax bracket and contribute $10,000, you reduce your current tax bill by $2,400. That money grows tax-deferred for decades, and you only pay taxes when you withdraw it in retirement—ideally when you’re in a lower tax bracket.

Roth accounts work differently: no upfront deduction, but all growth and withdrawals are completely tax-free after age 59½.

Over 30 years, the difference between paying taxes now (Roth) versus later (traditional) can be massive, depending on your current and future tax brackets.

The Employer Match: Free Money You’re Probably Leaving Behind

If your employer offers a 401(k) match, that’s the first place every dollar should go.

A typical match is 50% of your contributions up to 6% of your salary. On a $60,000 salary, that’s $1,800 in free money every year if you contribute at least $3,600.

Not contributing enough to get the full match is mathematically equivalent to accepting a pay cut.

Rebalancing and Fund Selection: The Hidden Performance Drag

Most 401(k) plans offer 15-30 fund choices, and most people pick randomly or just accept the default.

Target-date funds (like “2055 Retirement Fund”) are fine for hands-off investors, but they often charge 0.15-0.50% more than building your own three-fund portfolio.

A basic three-fund portfolio:

- U.S. total stock market index: 60%

- International stock market index: 30%

- Total bond market index: 10%

This is adjusted based on age and risk tolerance, but it’s a reasonable starting point for someone in their 30s-40s.

Contribution Limits Are Rising—Use Them

Contribution limits increase periodically to account for inflation.

For 2026, the limits mentioned earlier ($23,000 for 401(k)s, $7,000 for IRAs) represent significant opportunity—but only if you actually use them.

If you can’t max out immediately, increase contributions by 1-2% each year. Most people don’t notice the reduced paycheck, and over time, you reach the maximum.

What If You’re Behind on Retirement Savings?

If you’re in your 40s or 50s and haven’t saved much, don’t panic—but do act aggressively.

Catch-up contributions (available at age 50) allow an extra $7,500 in 401(k)s and $1,000 in IRAs. Use them.

Consider delaying retirement by 2-5 years. This gives you more contribution years, more compounding time, and reduces the number of years you need savings to cover.

Work with a financial planner to model realistic retirement scenarios. Hoping everything works out is not a plan.

Quick Summary

- Employer 401(k) match is the highest-return investment available

- Traditional vs. Roth choice depends on current and future tax brackets

- Most people can save 0.15-0.50% annually by choosing low-cost index funds

- Contribution limits increase over time—take advantage of them

- Starting late requires higher savings rates and potentially delayed retirement

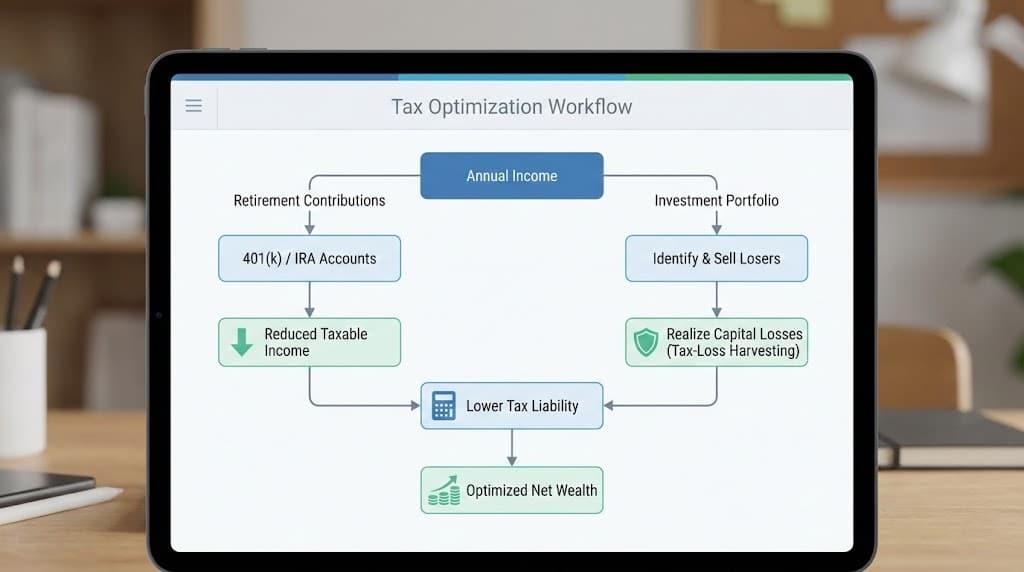

Step 4: Optimize Your Tax Position Early in the Year

Tax planning is one of the most controllable parts of financial strategy, and it’s consistently underutilized.

Most people think about taxes in March and April when filing. That’s too late to optimize.

The decisions you make in January through November determine your tax outcome for the year. To achieve financial freedom in 2026, you need to treat tax efficiency as an ongoing process, not a year-end scramble.

Tax-Loss Harvesting: Turning Losses Into Future Savings

If you have investments in taxable brokerage accounts, tax-loss harvesting lets you offset gains with losses.

When a stock or fund drops in value, you can sell it to realize the loss, then immediately buy a similar (but not identical) investment to maintain your market exposure.

This loss offsets up to $3,000 of ordinary income per year, and any excess carries forward to future years.

Example: You have $5,000 in capital gains and $8,000 in capital losses. The losses offset all gains, plus $3,000 of your ordinary income, reducing your tax bill by roughly $720-$1,100 depending on your bracket.

Wash sale rule: You can’t buy the same security within 30 days before or after selling it for a loss. This is where “substantially identical” matters—you have to switch to a different fund or wait 31 days.

Maximizing Tax Credits and Deductions

Tax credits reduce your tax bill dollar-for-dollar, making them more valuable than deductions.

Saver’s Credit: If your income is under $76,500 (married filing jointly) or $38,250 (single), you can get a tax credit worth 10-50% of your retirement contributions, up to $1,000-$2,000 depending on income level.

Most people miss this entirely because they don’t know it exists.

Retirement contribution deductions: Every dollar you put into a traditional 401(k) or IRA reduces your taxable income by that amount. At the 22% tax bracket, a $5,000 contribution saves you $1,100 in taxes.

HSA Triple Tax Advantage: The Most Underused Account

Health Savings Accounts (HSAs) are available if you have a high-deductible health plan.

They offer three tax benefits:

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals for qualified medical expenses are tax-free

No other account offers this combination.

2026 contribution limits: $4,300 (individual), $8,550 (family), plus $1,000 catch-up if age 55+.

The best strategy: pay current medical expenses out-of-pocket if possible, let your HSA grow for decades, then use it tax-free in retirement when medical costs are highest.

Estate Planning and Gift Tax Exclusions

If you’re building significant wealth, transferring assets efficiently to family members matters.

Annual gift tax exclusion (2026): $19,000 per person per year. You can give this amount to as many people as you want without filing any gift tax forms.

Married couples can combine their exclusions: $38,000 per recipient per year.

Lifetime estate tax exemption (2026): Approximately $13.99 million per individual. Most people won’t hit this, but if you might, work with an estate attorney now—exemption amounts can change with new tax legislation.

Step-by-Step Tax Optimization Guide

Follow this sequence at the start of each year:

1. Review last year’s tax return. Identify your marginal tax bracket and effective tax rate. This determines which strategies make sense.

2. Maximize retirement contributions. Adjust payroll deductions to hit annual limits if possible.

3. Set up quarterly tax-loss harvesting reviews. March, June, September, December. Harvest losses when they appear, don’t wait until year-end.

4. Calculate your HSA contribution strategy. If you have a qualifying health plan, max this account before taxable investing.

5. Review itemized vs. standard deduction. The standard deduction is $29,200 (married) or $14,600 (single) for 2026. Unless your mortgage interest, state taxes, and charitable giving exceed this, itemizing doesn’t help.

6. Plan charitable contributions strategically. If you’re close to the itemized deduction threshold, bunching multiple years of donations into one year can make itemizing worthwhile.

This is basic tax optimization. Complex situations—business income, real estate investments, stock options—require professional tax advice.

Quick Summary

- Tax planning happens year-round, not just at filing time

- Tax-loss harvesting can save $720-$1,100+ annually in taxable accounts

- Saver’s Credit is free money if your income qualifies

- HSAs offer triple tax advantages and should be maxed before taxable investing

- Estate planning and gift exclusions matter for wealth transfer

Step 5: Get Your Household Finances Running Smoothly

Financial freedom requires that your day-to-day money management isn’t a source of stress or inefficiency.

Small fixes in how you handle mortgages, debt, insurance, and automation can free up hundreds or thousands of dollars per year—and more importantly, reduce the mental load of managing money.

Mortgage Review: Refinancing and Rate Optimization

Mortgage rates fluctuated significantly from 2020-2025, and many homeowners locked in rates that may no longer be optimal.

When refinancing makes sense:

- You can lower your rate by at least 0.75-1.00%

- You plan to stay in the home long enough to recoup closing costs (typically 2-4 years)

- Your credit score has improved since your original mortgage, qualifying you for better terms

When refinancing doesn’t make sense:

- Rates have increased since your original mortgage

- You’re planning to move within 2-3 years

- Closing costs exceed your expected savings

Run the math before assuming refinancing is beneficial. Use mortgage calculators that account for closing costs and break-even timelines.

Eliminating High-Cost Debt: The Math That Matters

Credit card debt at 20-24% APR is an emergency, not a “normal” part of household finances.

If you’re carrying $10,000 in credit card debt at 22% APR, you’re paying $2,200 per year in interest alone. That’s $2,200 that could be going toward your emergency fund or investments.

Debt payoff sequence:

- Credit cards and payday loans (highest rates)

- Personal loans (moderate rates)

- Auto loans (lower rates)

- Student loans (often lowest rates, plus possible tax deduction)

- Mortgage (typically lowest rate, plus tax benefits)

Pay minimums on everything except the highest-rate debt, then attack that with every extra dollar until it’s gone. Then move to the next highest rate.

This is the mathematically optimal approach. The “debt snowball” method (smallest balance first) works for psychological reasons, but costs more in interest.

Insurance Review: Coverage Levels and Cost Efficiency

Insurance is essential protection, but most people either under-insure or over-insure.

Life insurance: If you have dependents, you need term life insurance equal to 10-12x your annual income. A $500,000 policy for a healthy 35-year-old costs roughly $25-$40 per month.

Whole life and universal life policies cost 8-12x more and are rarely the right choice for most families. Term life covers the years when your family actually needs income replacement.

Disability insurance: If your income supports your household, you need disability coverage. Most employer policies only cover 60% of income and are taxable. Private policies can fill the gap.

Auto and homeowners insurance: Review these annually. Bundling saves 10-25%. Increasing deductibles from $500 to $1,000 can reduce premiums by 15-30%. Just make sure your emergency fund can cover the higher deductible.

Automating Savings and Investments

Automation removes willpower from the equation.

Set up automatic transfers:

- Emergency fund contribution: the day after payday

- 401(k) contribution: through payroll deduction

- IRA contribution: monthly auto-transfer from checking

- Taxable brokerage contribution: monthly auto-transfer

When these transfers happen automatically, you build wealth by default rather than by remembering to do it manually.

Fee Audits: Where Your Money Leaks Without You Noticing

Small recurring fees add up to thousands of dollars per year.

Common money leaks:

- Bank account monthly fees: $12-$25/month = $144-$300/year

- ATM fees: $3-$5 per transaction

- Investment account fees: 0.50-1.50% annually on your entire balance

- Subscription services you don’t use: $10-$50/month = $120-$600/year

Audit your bank and credit card statements quarterly. Cancel unused subscriptions. Switch to no-fee bank accounts. Move investments to low-cost index funds.

A $100,000 investment portfolio charging 1.00% in fees costs you $1,000 per year. The same portfolio in a 0.03% index fund costs $30 per year. Over 30 years, this difference compounds to over $100,000 in lost returns.

Practical Tool: Monthly Cash Flow Template

Track your actual spending for one month, then use this framework:

Income

- After-tax salary

- Side income

- Investment income Total monthly income: $_____

Essential Expenses (50-60% of income)

- Housing

- Utilities

- Groceries

- Insurance

- Minimum debt payments Total essential: $_____

Financial Goals (20-30% of income)

- Emergency fund contribution

- Retirement contributions

- Debt payoff above minimums

- Taxable investing Total financial goals: $_____

Discretionary Spending (20-30% of income)

- Dining out

- Entertainment

- Travel

- Hobbies Total discretionary: $_____

If your percentages are significantly off from these ranges, adjust. You can’t achieve financial freedom in 2026 or beyond if 80% of your income goes to expenses and only 5% goes to financial goals.

Quick Summary

- Mortgage refinancing only makes sense if you save 0.75-1.00% and stay long enough to recoup costs

- High-rate debt (credit cards, payday loans) is a financial emergency requiring aggressive payoff

- Term life insurance covers income replacement needs at 8-12x lower cost than permanent policies

- Automation removes willpower from saving and investing

- Fee audits can recover $500-$2,000+ per year in leaked money

Step 6: Create a Financial Plan to Achieve Financial Freedom 2026

Everything covered so far—emergency funds, investing, retirement accounts, tax optimization, household efficiency—needs to connect into a coherent long-term roadmap.

That’s what a financial plan does.

Most people don’t have one. They save when they remember, invest sporadically, and hope everything works out. This approach rarely leads to financial freedom.

A real financial plan connects your current financial situation to your specific goals with realistic timelines and measurable milestones.

What a Financial Plan Actually Includes

A complete financial plan addresses:

1. Net worth tracking: Assets minus liabilities, updated quarterly or annually. This is your core financial health metric.

2. Cash flow management: How much comes in, where it goes, and whether you’re living within your means while still funding long-term goals.

3. Debt elimination timeline: Specific payoff dates for each debt, prioritized by interest rate.

4. Emergency fund target and timeline: 3-6 months of expenses, with monthly contribution amounts and expected completion date.

5. Retirement savings projections: How much you need to retire comfortably, how much you’re contributing now, and whether you’re on track to hit your target by your desired retirement age.

6. Investment allocation strategy: What percentage goes to stocks vs. bonds, domestic vs. international, and how this changes as you age.

7. Tax optimization strategy: Which accounts to prioritize, when to do tax-loss harvesting, and how to minimize lifetime tax burden.

8. Insurance coverage review: Life, disability, health, property—adequate coverage without over-insuring.

9. Estate planning basics: Will, power of attorney, healthcare directives, and beneficiary designations.

This sounds overwhelming, but you don’t build it all at once. You build it step by step, starting with the highest-impact areas first.

The 5-Year Financial Freedom Roadmap

Most people underestimate how long meaningful financial progress takes.

To achieve financial freedom in 2026, you’re really starting a 5-10 year journey. Here’s what realistic timelines look like:

Year 1 (2026):

- Establish 1-2 months emergency fund

- Start consistent monthly investing

- Get employer 401(k) match

- Eliminate highest-rate debt

- Build basic budget tracking

Year 2:

- Complete 3-6 month emergency fund

- Increase retirement contributions by 2-3%

- Pay off remaining high-rate debt

- Implement tax-loss harvesting if applicable

- Annual insurance review

Year 3:

- Emergency fund fully funded

- Retirement contributions at 15-20% of income

- All consumer debt eliminated

- Begin taxable investing if retirement accounts maxed

- Estate planning documents completed

Years 4-5:

- Consistent investment habit fully automated

- Retirement accounts on track for age-based targets

- Only low-rate debt remaining (mortgage, maybe student loans)

- Net worth growing primarily from investment returns, not just contributions

- Financial plan reviewed and adjusted annually

This is a realistic pace for someone starting from a moderate financial position. If you’re further behind, the timeline extends. If you’re ahead, you can accelerate.

When to Hire a Financial Advisor

You don’t need an advisor to follow basic principles, but professional guidance adds value in specific situations:

You should consider hiring help if:

- Your net worth exceeds $500,000 and tax optimization becomes complex

- You’re within 5-10 years of retirement and need distribution planning

- You have stock options, RSUs, or other complex compensation

- You own a business and need integrated personal/business planning

- You’re going through major life changes (inheritance, divorce, job loss)

- You simply don’t want to manage this yourself and prefer delegation

Fee-only advisors charge either hourly rates ($150-$400/hour), flat annual fees ($2,000-$10,000), or a percentage of assets (0.50-1.50% annually). Fee-only advisors don’t earn commissions on products, which reduces conflicts of interest.

Robo-advisors like Betterment, Wealthfront, or Vanguard Digital Advisor charge 0.15-0.50% annually and handle investment management automatically. They work well for straightforward situations but can’t provide comprehensive tax or estate planning.

The Biggest Planning Mistake: Not Adjusting as Life Changes

Your financial plan isn’t static.

Major life events require plan updates:

- Marriage or divorce

- Children

- Job change or income increase

- Inheritance

- Home purchase

- Health issues

- Market crashes or booms

Review your plan formally once per year. Make minor adjustments quarterly if needed. The plan guides you, but it shouldn’t be rigid to the point of ignoring reality.

Practical Tool: Annual Financial Review Checklist

Copy and complete this every January:

Net Worth

- Total assets: $_____

- Total liabilities: $_____

- Net worth: $_____

- Change from last year: _____%

Emergency Fund

- Current balance: $_____

- Target balance: $_____

- Progress: _____%

Retirement Accounts

- 401(k) balance: $_____

- IRA balance: $_____

- Contribution rate: _____%

- On track for retirement goal? Yes / No

Debt

- Total remaining debt: $_____

- Highest interest rate: _____%

- Projected payoff date: _____

Insurance

- Life insurance coverage: $_____

- Disability coverage: $_____

- Last review date: _____

Investments

- Total invested: $_____

- Asset allocation: ___% stocks, ___% bonds

- Rebalancing needed? Yes / No

Action Items for This Year

This annual review keeps you accountable and ensures you’re making actual progress, not just staying busy with financial tasks that don’t move the needle.

Quick Summary

- A financial plan connects current actions to long-term goals with measurable milestones

- Realistic financial freedom timelines are 5-10 years, not 6 months

- Year 1 focus: emergency fund, consistent investing, employer match, high-rate debt

- Professional advice adds value for complex situations or when approaching retirement

- Annual reviews ensure your plan stays aligned with life changes

Final Thoughts: Financial Freedom Is Built, Not Found

The path to achieve financial freedom in 2026 isn’t about discovering a secret strategy or getting lucky with a single investment.

It’s about executing fundamental financial principles consistently over years.

Emergency funds provide stability. Monthly investing builds wealth. Retirement accounts maximize tax efficiency. Smart household management prevents money leaks. A clear plan ties everything together.

Most people overestimate what they can accomplish in one year and underestimate what they can accomplish in ten years. This is true in nearly every area of life, but it’s especially true with money.

What realistic progress looks like:

- In 6 months: emergency fund started, automatic investing established, high-rate debt reduced

- In 1 year: emergency fund at 2-3 months, retirement contributions increased, financial plan drafted

- In 3 years: emergency fund complete, retirement on track, consumer debt eliminated

- In 5 years: net worth growing from investment returns, financial freedom roadmap visible

- In 10 years: substantial wealth accumulated, retirement goals achievable, financial stress minimal

The work you do in 2026 sets up 2027. The work you do in 2027 sets up 2028. Compounding applies to habits as much as it applies to investments.

Start with one step. Build the emergency fund. Automate the monthly investment. Get the employer match. Then add the next step.

Financial freedom comes from consistent, purposeful action—not from waiting for the perfect moment to start.

Final reminder: This guide is educational only. Individual financial decisions should be made in consultation with qualified financial professionals who understand your complete situation. All investments carry risk, and past performance does not guarantee future results.